This content represents the writer’s opinions and research and is not intended to be taken as financial advice. The information presented is general in nature and may not meet the specific needs of any individual or entity. It is not intended to be relied upon as a professional or financial decision-making tool.

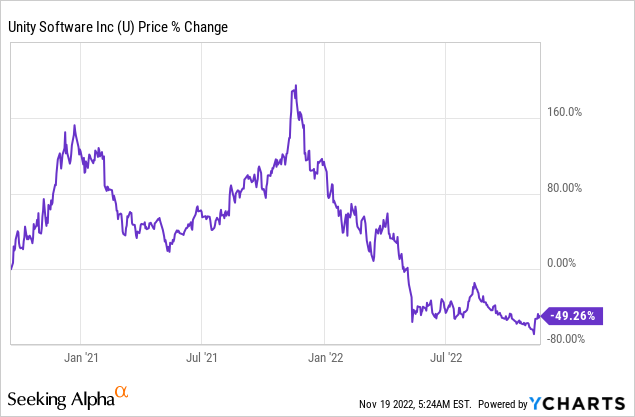

Unity Technologies went public in 2020 and the stock’s price is almost 50% down since the IPO.

Considering the growth prospects of the company and the current valuation, one may wonder how the price will behave in the future.

In this article, we will discuss what Wall Street analysts think about that and whether it’s in touch with reality. Then, we will examine how Unity’s price has behaved in the past and why.

But first, you need to know how the company makes money…

Table of Contents

Business Overview of Unity Technologies

Unity Software Inc. (doing business as Unity Technologies), founded in Copenhagen and headquartered in San Francisco, provides a licensed game engine called Unity.

The company was founded by David Helgason, Joachim Ante, and Nicholas Francis in 2002, but it wasn’t incorporated until 2004 as Over The Edge Entertainment. In 2007, it changed its name to Unity Software Inc.

Unity’s game engine allows users to develop 3D and 2D games and applications. The use of Unity is not confined to just game developers, however. Instead, it has been used in other industries such as film production, engineering, construction, automotive, architecture, and the US Armed Forces.

Unity’s success is based on its design. Its development is intended to support different platforms. It is now used to design games and other applications across more than 25 platforms (i.e. consoles, desktop, mobile, VR, AR, etc.).

Unity Technologies monetizes its software in 3 ways:

- Subscriptions

Anyone can create an account and use the engine for free. But companies that want advanced features and take Unity’s name off of their games need to pay a monthly subscription. - Monetization Tools

Unity also provides developers with tools to monetize their games through in-app purchases and ads. The company uses a revenue-share model to monetize such tools. - Developer Tools

In addition, the company sells developers software that help them support player communication, analytics, or content delivery. Some games need such tools so they work better online and enable developers to continually update them.

Unity Stock Forecast 2023

Unity (U) doesn’t have a long trading history, so it’s still early to confidently predict where the stock price is headed.

But Wall Street’s median price target of $36 per share suggests a 12-month 9.8% upside from the current price. This target captures the information we have about the company so far.

First, let’s talk about some qualitative aspects of the business.

One important thing that cannot be ignored when we analyze tech-based businesses is management quality. Early on, Unity’s managers showed signs they can adapt fairly fast in order to succeed.

The company released its first game, GooBall, as Over The Edge Entertainment in 2005, but failed commercially. However, founders quickly shifted their efforts into commercializing their game development tools they had created to simplify game development, in which they saw value.

Another much later notable move was adding John Riccitiello as CEO in 2014. Riccitiello’s background included running Electronic Arts and co-founding the private equity firm Elevation Partners.

After he was onboard, he oversaw two fundraising rounds for the company, raising $181 million in 2016 and $400 million in 2017. He has also worked on getting the game engine into Oculus’ software development kit.

On top of those, he led efforts to capture a wider audience by making Unity’s software tools accessible for use in other industries (i.e filmmaking, automotive design, construction, etc.)

In 2018, in what seemed like an effort to compete with other software like Epic Games’ Unreal Engine, Unity created a team called the Unity Icon Collective. It is focused on creating assets like AAA art for sale in the Unity Asset Store.

All in all, Unity shows signs of determination to succeed and the way they were able to adapt to changing circumstances exhibits nothing but confidence.

However, the company’s financials tell another story…

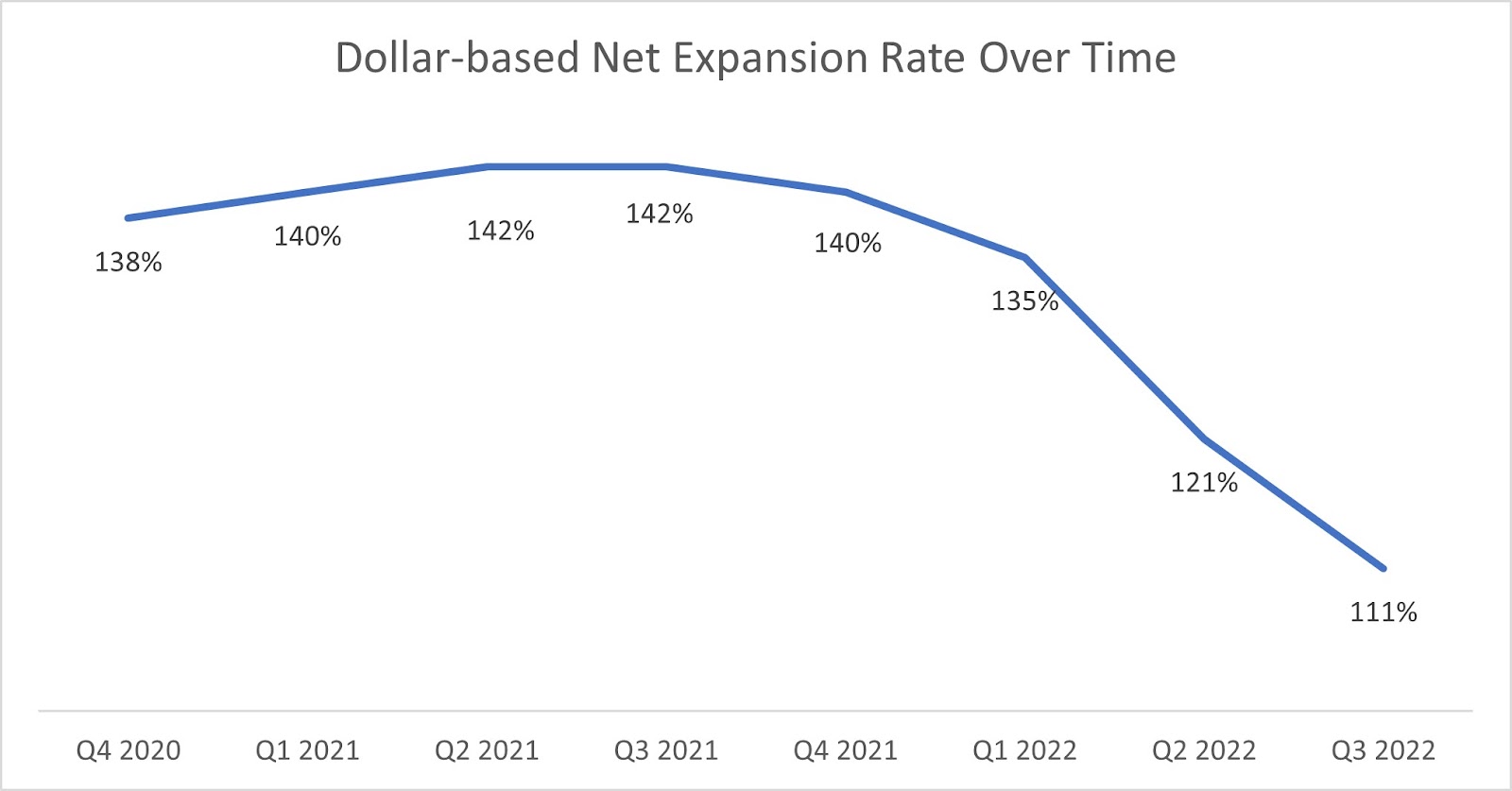

First of all, Unity’s latest quarterly report indicates a decline in its ability to upsell to its customers:

If you’re unfamiliar with the Dollar-Based Net Expansion Rate or DBNER, it simply measures how much revenue Unity was able to generate through selling additional services or products to existing subscribers within a given period.

For instance, in the last quarter, its DBNER was 111%. That means that by the end of the quarter, it had sold 11% more products to subscribers than at the start of the quarter.

As you can see in the graph above, the company’s profitability started falling at an accelerated pace around the first quarter of 2022. If the trend is maintained, market doubts around its ability to keep deriving increasing value from subscribers may have an adverse effect on its stock’s price.

Speaking of doubt, the company’s capital structure may be conservative but its cash burn is concerning.

It’s not so much the rate at which it invests its cash flow but how that is problematic. It has acquired a lot of other companies in order to expand throughout the last half of the previous decade.

Now, it’s completely normal for a company to do that to grow its business; especially in the tech industry. But Unity has been a serial acquirer for a while. In retrospect, such acquisitions may prove very valuable. But knowing that Unity has been operating at a loss for so long and that it lacks any tangible assets doesn’t help here.

No doubt, its nature as a tech business and its acquisition record has left shareholders with a negative tangible book value. Of course, if the company manages to ever be profitable, it may fix this. However, investing cannot be based on an “if”.

Speaking of profitability, revenue is growing but its income is declining. Based on Unity’s latest quarterly report, that’s mainly because of R&D expenses.

And the stock is still trading at a premium to book value (6.5 times) and revenue (8.2 times).For some context, the S&P 500 index is currently trading at 2.3 times the book value and 3.8 times the revenue.

Unity Stock 2022

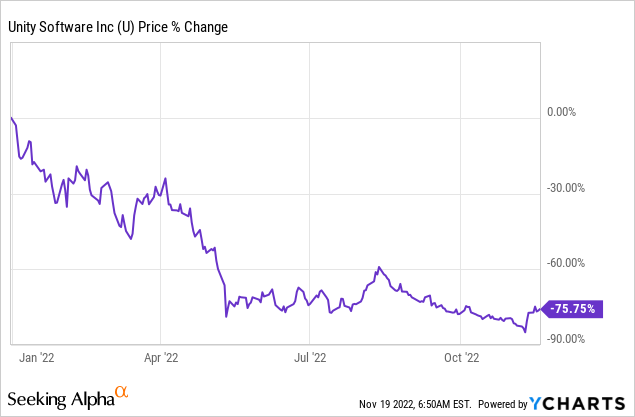

Unity lost more than 75% of its market value in 2022. The price of Unity slipped from above $130 in January to $30 as of December 2022. That mainly reflects a deteriorating performance compared to the previous years.

There were only two significant price increases.

First, during the period of November 10-18, the price increased by 61.3%. The market likely appreciated management’s expectation (Q3 results released on Nov. 9th) to generate a small profit for the 4th quarter (it would be the first in its operating history).

Second, on February 4th, Unity’s price went up by 17.42%, just one day after the company released its Q4 results, forecasting a much smaller earnings loss for the next quarter.

The dips, now. On July 13th, Unity fell by 17.45%, likely over news that it would acquire ironSource. It’s usual for prospective acquirers to lose market value after the announcement as a premium will often have to be paid for the acquisition.

At this point, it’s worth noting that such an acquisition may indeed prove fruitful. Applovin, a rival of ironSource proposed to merge with Unity if it dropped the merger negotiation with ironSource. This may be a clue regarding the threat to competitors like Applovin that such an acquisition would pose and the consequent value of the newly combined entity.

The Price also fell more dramatically on May 11th (-37.05%), a day after the company released its earnings results for its first quarter. While earnings seem to have met analyst expectations, Unity’s revenue and general outlook fell short.

Unity Stock 2021

In 2021, Unity’s price performance was flat(ish) overall (-6.83%). There was massive selling pressure at the year’s start, but the price started recovering to previous levels in the year’s second half.

Most of this price performance could be attributed to fundamentals. One day after the company released its results for its fourth quarter on February 4th, the stock fell by 14.13%. Its in-line guidance and soft revenue performance were likely disappointing to shareholders.

With that being said, there were some interesting developments later that year…

On August 11th, the company announced strong guidance and beat consensus expectations in Q2 earnings. The following day, the price was up 13.25%.

Similarly, on November 9th the price increased by 20.57%, just after Unity released its Q3 earnings.

Conclusion

Unity’s recent price performance seems to be starting to reflect its business fundamentals. But the price isn’t as low as it should be for a company losing money.

With that being said, if the price trend of this year continues, Unity could reach a more attractive valuation and be subject to purchase on an investment basis. For now, the price seems to reflect the market’s anticipation of possible outcomes, rather than the company’s financials.

For this reason, keeping track of this stock’s performance is definitely worth it.

Its acquisitions may have impaired shareholders’ equity but could prove profitable in the future. We know that at least one competitor was unsettled by Unity’s offer to buy ironSource recently. And that surely says something…

FAQ

Is Unity software overvalued?

Compared to the overall market, Unity seems to be overvalued. Since the company isn’t yet profitable, using the Price to Sales ratio makes sense. It’s currently at 8.2x. For context, the S&P 500 index has a P/S ratio of 2.2x, way below that of Unity.

Why did Unity stock drop so much?

Unity’s stock dropped by 75.75% YTD, likely because of unmet analyst expectations and the announced acquisition of ironSource. More precisely, there was high selling pressure after the proposed acquisition was announced (-17.45%) and the stock fell by an outstanding 37.05% after Unity released its Q1 results early this year.

Why is Unity not profitable?

Unity isn’t profitable yet because it seems to be having a lot of Research & Development expenses. Aggressive investing in future growth is common for tech stocks. However, Unity’s profitability witnessed a decline recently (The dollar-Based Net Expansion Rate was only 111% for Q3), which may be a contributing factor here.

WeInvests is a financial portal-based research agency. We do our utmost best to offer reliable and unbiased information about crypto, finance, trading and stocks. However, we do not offer financial advice and users should always carry out their own research.

Read More